.jpg)

Key Takeaways

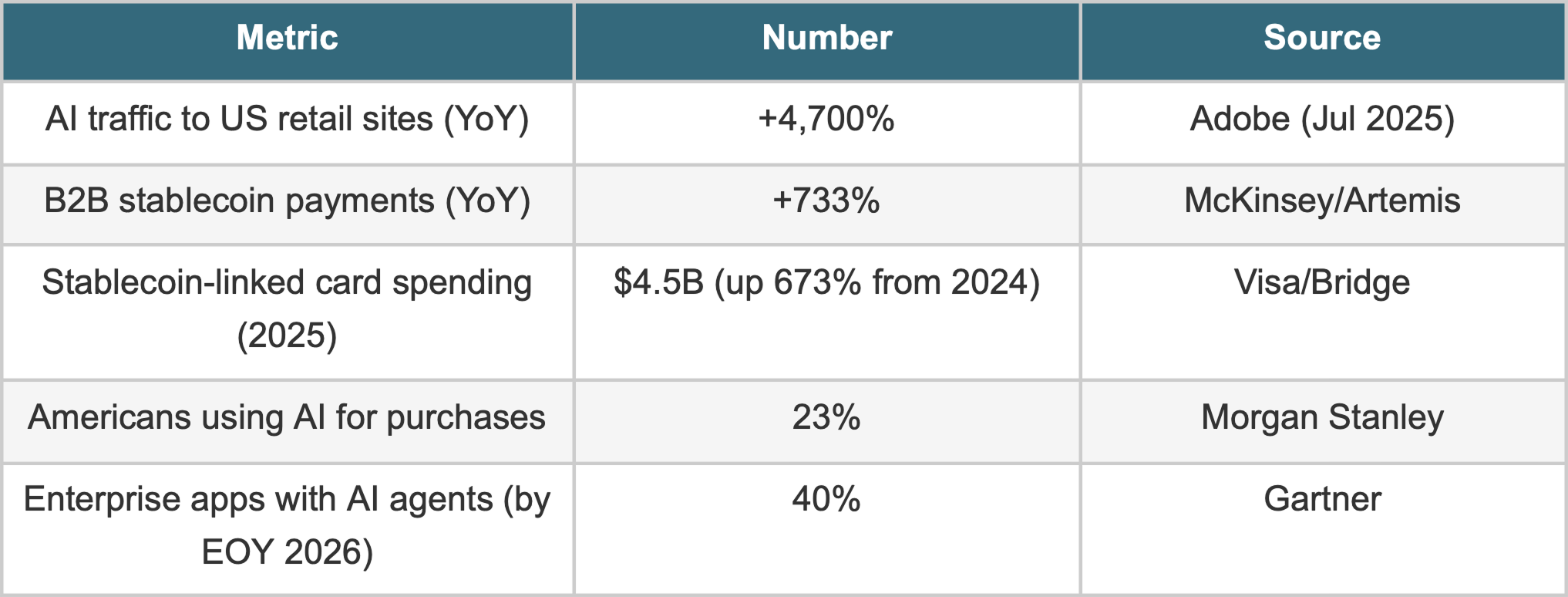

- Agentic commerce is not a future state. AI-assisted purchasing already influenced $3B in US Black Friday sales (Salesforce). One in five Cyber Week 2025 orders involved an agent. OpenAI, Google, Stripe, and PayPal all shipped agent commerce infrastructure in the past 90 days.

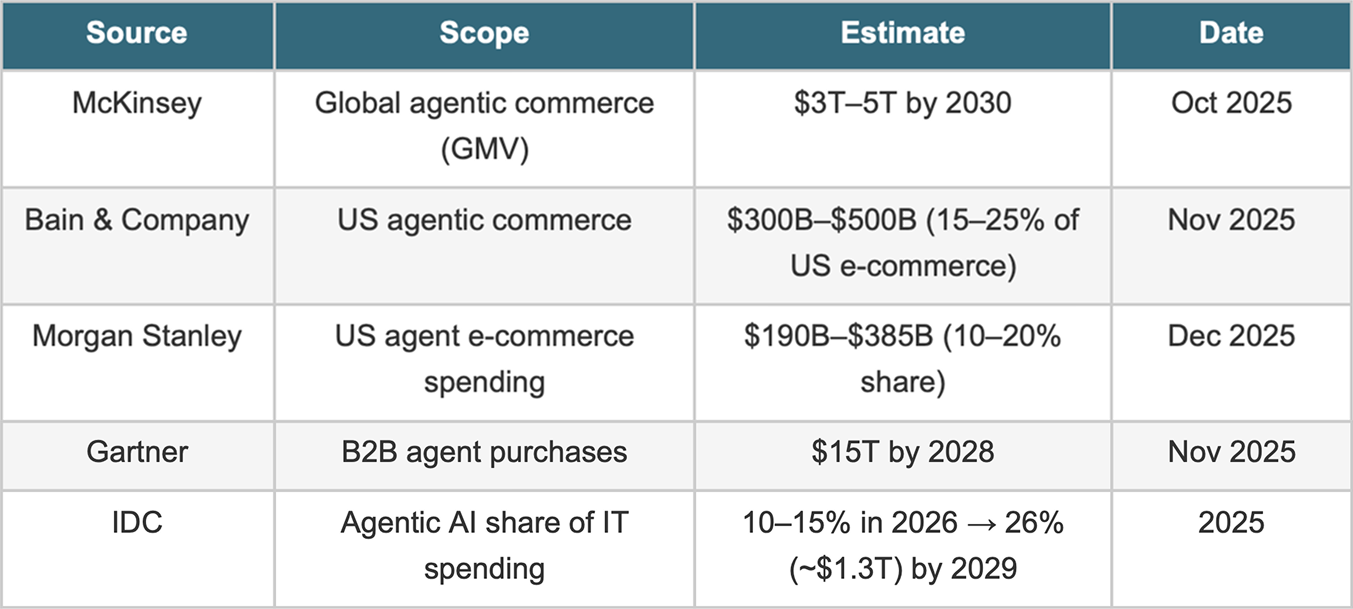

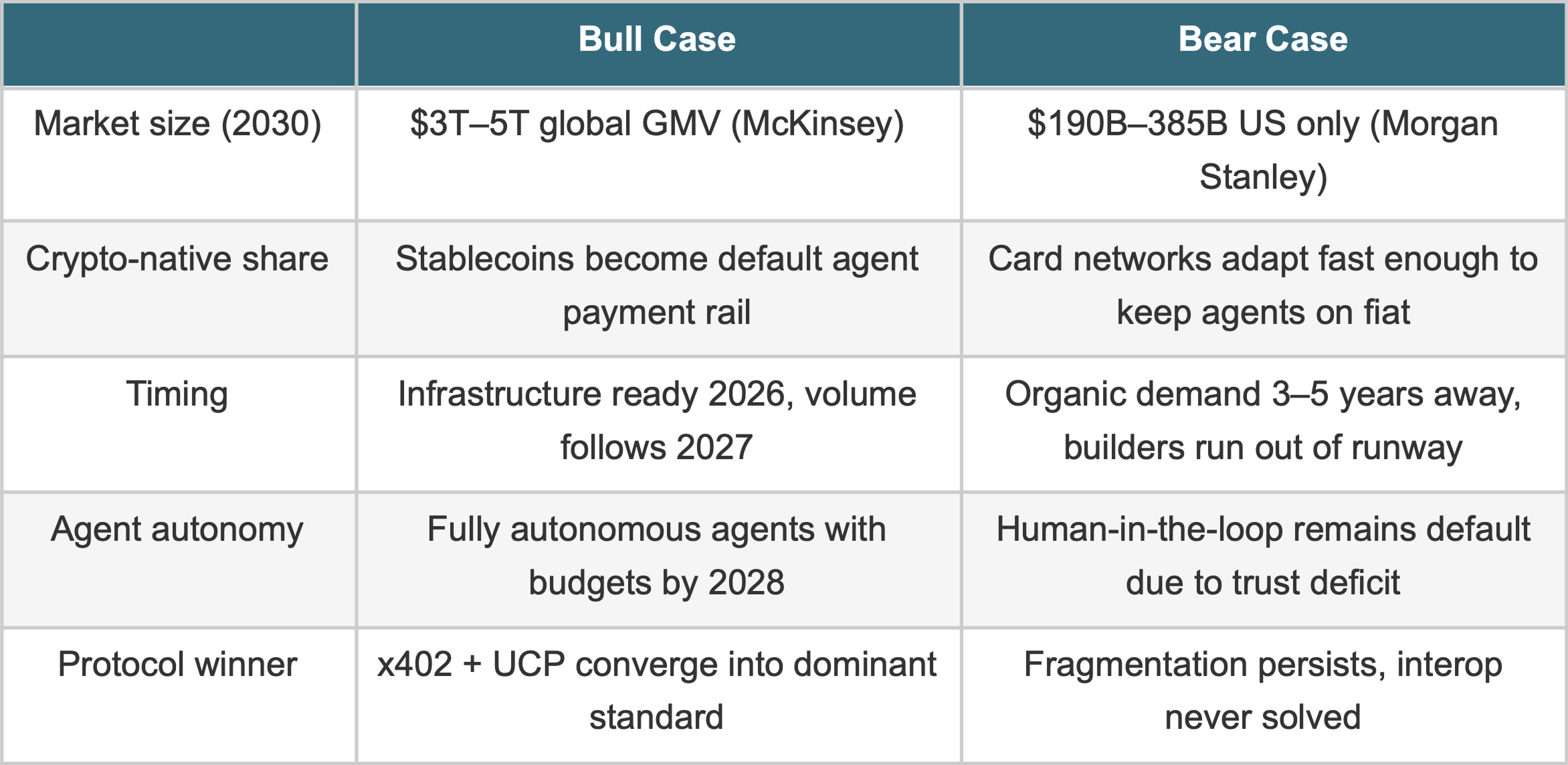

- Analyst consensus on direction is unusually strong for an early-stage market. McKinsey's bull case is $3–5T in global agentic GMV by 2030. Morgan Stanley's bear case is $190–385B in US agent e-commerce alone. The variance is on magnitude and timing, not on whether the shift occurs.

- The stack is forming fast but fragmented. Three competing payment protocol families (x402, MPP, UCP/AP2) plus KYAPay, three wallet standards, multiple execution environments. No dominant vertical integration. Protocol fragmentation is the primary near-term adoption risk. This is 2015 cloud infrastructure.

- Traditional payment rails are architecturally incompatible with Agent-to-Agent commerce. Agents cannot pass KYC. Card network fee structures make sub-$0.30 micropayments economically unviable. Stablecoins are not a preference, they are the only viable settlement layer for agent-to-agent transactions at any meaningful frequency.

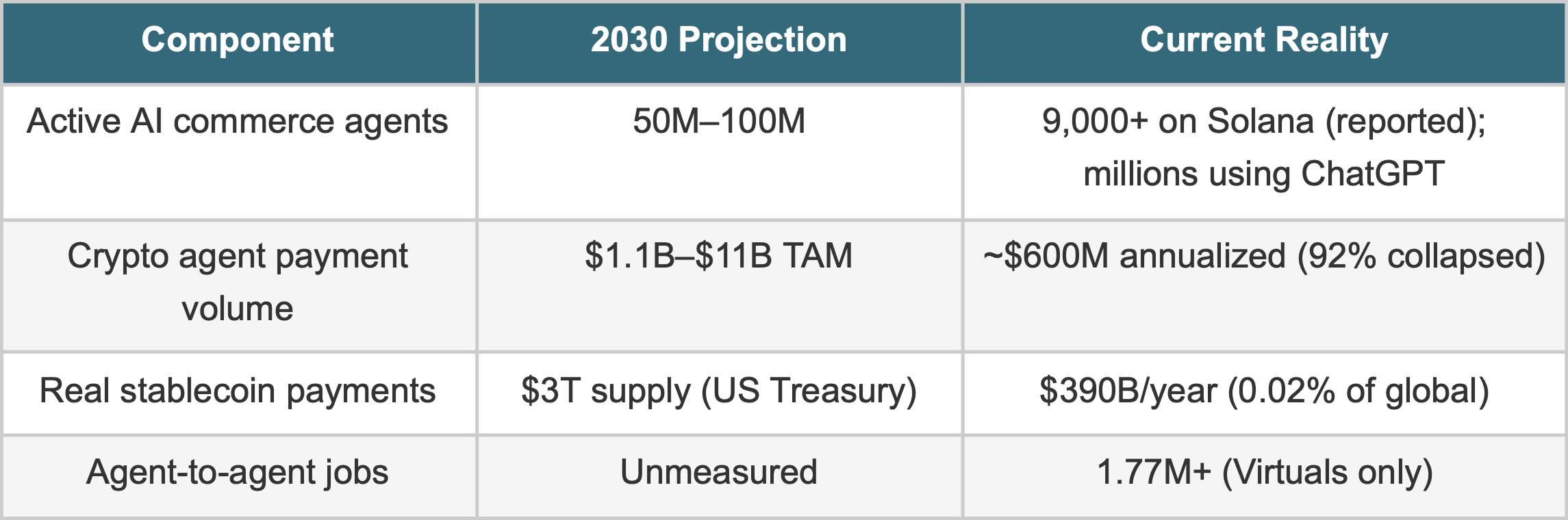

- Crypto-native agent payment volume is negligible and mostly non-organic. x402 volume collapsed 92% between December 2025 and February 2026. Real agent-to-agent service revenue across the largest marketplace is $2.63M. The structural thesis is high conviction. The timing thesis is not.

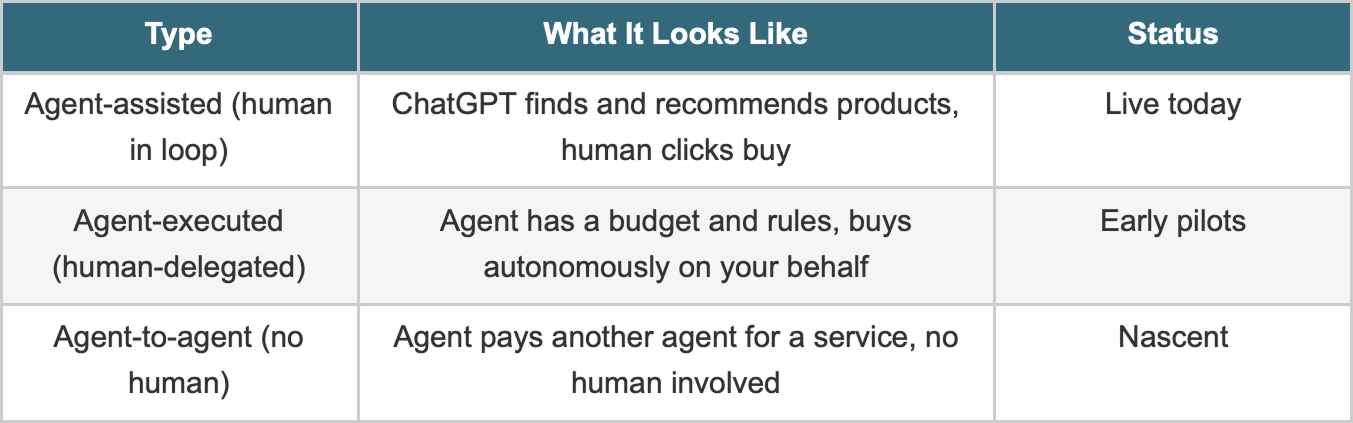

1. Agents Aren't Just Shopping. They're Building Their Own Economy.

Agentic commerce describes the paradigm shift from human-led buying decisions to AI systems that not only recommend the purchases but execute them. AI-assisted shopping already accounted for $3B in US Black Friday sales (Salesforce). One in five Cyber Week orders involved AI-powered recommendations or conversational service. Now we are moving into purchasing flows where agents not only recommend, but find the product, compares prices across stores, negotiates a discount, pays and tracks delivery. Consumer shopping is just one layer. Underneath, an even more important shift is happening: agents are starting to pay other agents. For data scraping, compute, content generation, brand design.

The question is no longer if agents will handle commerce. It's how they'll pay for things, a question that is restructuring payments, identity, and execution infrastructure from the ground up.

Three distinct commerce modalities are developing in parallel, each with different infrastructure requirements:

Consumer-facing commerce (type 1) is largely solved by existing rails: Shopify, PayPal, Visa. Agent-delegated and agent-to-agent commerce require purpose-built infrastructure. That buildout is what this report covers.

2. Every Major Analyst Agrees: Multi-Trillion Dollar Shift

Analyst consensus on direction is unusually strong for an early-stage market. The variance is on magnitude and timing, not on whether the shift occurs.

Actual stablecoin payments are ~$390B annually. That's 0.02% of global payment volume. The growth is compounding off a tiny base. The timing is uncertain, the direction is not.

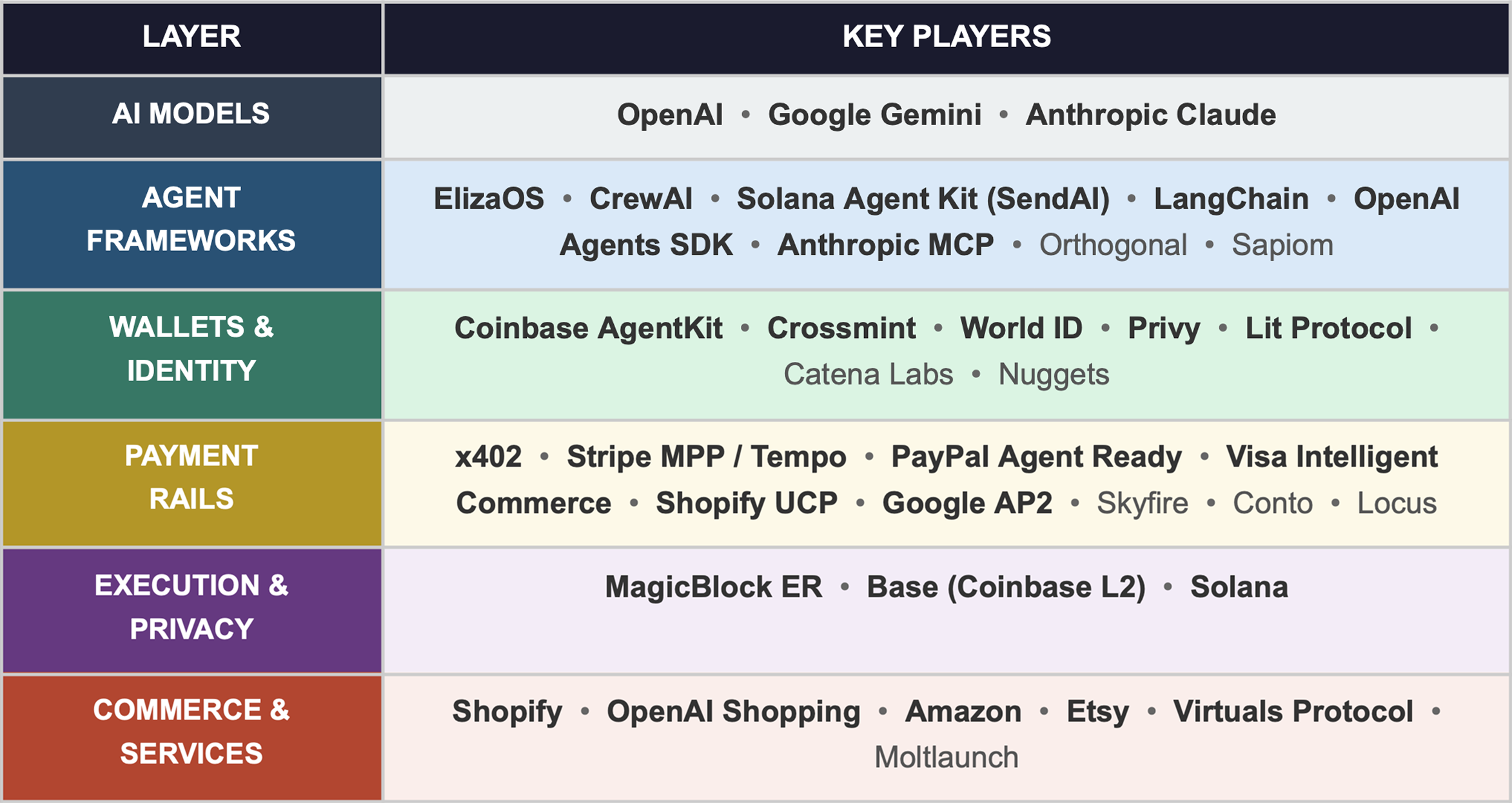

3. No One Owns the Stack Yet

This is the infrastructure being built right now. The agent stack is modular and still forming. No single player owns more than two layers.

Bold = established players | Regular = emerging players

Layer 1 — AI Models: The raw intelligence. These models handle planning, decision-making, and task execution behind every agent workflow. The layer is effectively consolidated with OpenAI, Google, and Anthropic accounting for the vast majority of production deployments.

Layer 2 — Agent Frameworks: The orchestration layer that turns models capability into agents that can take actions in the real world like browsing, transacting, communicating, coordinating. More fragmented than layer 1, with specialization emerging by chain and use case. ElizaOS (90+ plugins), CrewAI (pre-built tool ecosystem), Solana Agent Kit / SendAI (60+ pre-built Solana actions), LangChain (200M+ monthly PyPI downloads), OpenAI Agents SDK (native commerce via ACP).

Layer 3 — Wallets and Identity: Agents need to hold funds, sign transactions, and prove authorization without human intervention at every step. This layer is solving a problem traditional finance never had to: issuing financial identity to non-human entities. Coinbase AgentKit (wallet + identity bundle), Crossmint Smart Wallets (dual-key architecture, on Squads Protocol), Privy (embedded wallets), Lit Protocol (Programmable signing), Catena Labs ($18M seed, a16z, Circle co-founder).

Layer 4 — Payment Rails: How agents actually move money. The most actively contested layer in the stack, with three competing protocol families and no clear winner. Protocol outcome here determines which chains and wallets win by default. x402 (Coinbase/Cloudflare, HTTP-native micropayments), Stripe MPP / Tempo (mainnet Mar 18, 2026), Google UCP + AP2 (co-developed with Shopify, 60+ partners), Skyfire KYAPay (agent identity + spending limits, live since Dec 2024). Visa Intelligent Commerce is integrating across protocols (MPP, KYAPay) rather than competing with its own standard.

Layer 5 — Execution: Where transactions run. For single payments, any chain works. For multi-step agent-to-agent flows throughput, cost, and privacy become the differentiating variables. MagicBlock Ephemeral Rollups (private, elastic, sub-50ms, zero fees), Base (sub-cent transactions, ~200ms finality, x402 native chain), Solana mainnet (~$0.00025/txn, ~400ms, 9,000+ agents registered).

Layer 6 — Commerce and Services: The counterparties and merchants with whom the agents actually transact. Consumer-facing commerce (Shopify, Etsy, Amazon) is integrating agent-assisted checkout now. Agent-to-agent commerce (Virtuals Protocol ACP) is the more structurally novel category, software buying from software with no human in the loop. Shopify (Agentic Storefronts, all stores live on ChatGPT), Etsy (Instant Checkout via OpenAI live), Amazon (OpenAI Strategic partnership, Rufus AI Shopping), Virtuals Protocol ACP (1.77M+ jobs, $2.63M monthly agent revenue).

Stack assessment: Four competing payment protocols. Three wallet standards. Multiple execution environments. No dominant vertical integration. Protocol fragmentation is the primary adoption risk at this layer. This resembles 2015 cloud infrastructure: the right primitives exist, consolidation has not occurred.

So What?

The stack is forming fast but fragmented. Four competing payment protocols (x402, MPP, UCP, KYAPay), three wallet standards, multiple execution environments. No dominant stack yet. Whoever assembles the best vertical integration wins. This is 2015 cloud infrastructure all over again.

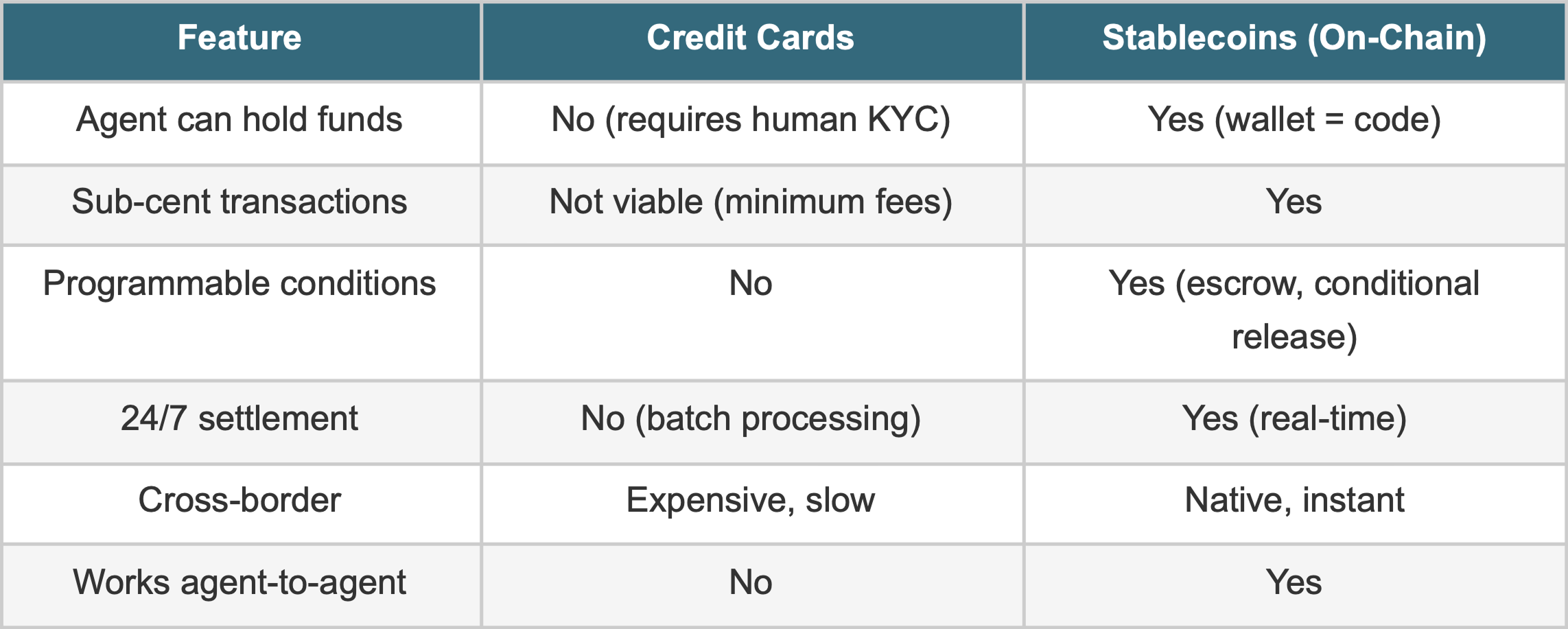

4. Card Networks Can’t Process a $0.01 Transaction

There are structural limitations of traditional payment systems when applied to autonomous software.

Problem 1: Agents can't open bank accounts. An AI agent can't pass KYC. It can't hold a credit card because it doesn’t have a legal identity. Traditional finance assumes a human on both sides of every transaction. Agents break that assumption.

Problem 2: Card fees kill micropayments. Every card transaction carries a fixed processing fee (typically $0.05–$0.15 per swipe) on top of the percentage-based fee. This fixed fee goes to the issuing bank as part of interchange and exists regardless of the transaction size. On a $50 purchase, it's invisible. But when an agent makes 500 API calls at $0.01 each, that fixed fee applies to every single transaction: 500 × $0.05 = $25 on the low end, 500 × $0.15 = $75 on the high end. The total service cost is only $5 (500 × $0.01), meaning processing fees alone are 5–15x the value of the services purchased. The percentage-based fee (2–3% of $0.01) is negligible at this scale. it's the per-swipe minimum that makes the entire category of micropayments structurally uneconomical on card rails. By contrast, a USDC transfer on Solana costs roughly $0.0005 per transaction, with no fixed minimum compared with the same 500 calls would cost $0.24 in total fees.

Problem 3: Agents need programmable money. An agent hiring another agent needs escrow (pay when the job is done), conditional release (pay only if output meets criteria), and refund logic. Credit cards can't programmatically do this, but smart contracts can.

So What?

Crypto rails aren't a preference. They're a structural requirement for agent-to-agent commerce. Card networks were built for humans buying things from stores. Agent commerce needs programmable, identity-light, fee-light money. Stablecoins are the only option that exists today.

5. Consumer Commerce Is Real. Crypto-Native Payments Are Not.

What's Real (Live, Measurable)

Consumer AI-assisted shopping is happening. AI-powered recommendations and conversational service influenced $3B in US Black Friday sales (Salesforce). During Cyber Week 2025, one in five orders involved AI-assisted product discovery. 23% of Americans made purchases using AI in the past month (Morgan Stanley). OpenAI's Instant Checkout is live on Etsy. PayPal's Agent Ready is rolling out across AI surfaces. Note: these are AI-assisted purchases where humans still click buy, not fully autonomous agent transactions.

Agent-to-agent services are the earliest non-DeFi use case. Virtuals Protocol: 1.77M+ jobs completed, ~$2.6M in agent revenue (Jan 2026). These are agents paying other agents for data scraping, brand identity design, content generation. Not DeFi trades.

Developer momentum is strong. ElizaOS: ~17K stars in ~16 months. Solana Agent Kit: 100K+ downloads. 9,000+ agents reportedly registered on Solana. Solana/Colosseum AI Agent Hackathon (Feb 2026, $100K USDC). 40% of enterprise apps will include AI agents by end of 2026 (Gartner).

What's Still Narrative (Projected, Unproven)

Crypto-native agent commerce volume is tiny and mostly non-organic. x402 volume collapsed 92% from December 2025 to February 2026, with the vast majority of prior volume was non-organic. Actual agent spending on real goods and services via crypto rails is negligible..

Enterprise adoption has significant failure risk. 40%+ of agentic AI projects are at risk of cancellation by 2027 (Gartner). 69% of AI projects don't make it to live operational use (Blue Prism). ~50% of consumers are still cautious about agents handling purchases autonomously (Bain).

So What?

Consumer agentic commerce is real. Crypto-native agent payments are 12–18 months early. The infrastructure is being built (x402, MPP, UCP) but organic volume doesn't exist yet. Position based on structural inevitability, not current traction.

6. The Infrastructure May Arrive Two Years Before the Demand

Timing risk (high). Every infrastructure bet here assumes rapid agent commerce scaling. Stablecoin payments are 0.02% of global volume. x402 organic volume is effectively zero. The market could take 3–5 years longer than consensus projections. Infrastructure built now may sit idle for longer than operators can sustain.

Protocol fragmentation (medium-high). Multiple competing standards, none dominant. Without consolidation, developers face integration fatigue and agents face cross-protocol interoperability failures.

Consumer trust deficit (medium). Approximately 50% of consumers remain cautious about agents making purchases autonomously (Bain). One high-profile agent error like unauthorized purchase or a wrong item has the potential to set the delegated-commerce category back materially.

Enterprise project failure rate (medium). 40%+ of agentic AI projects face cancellation by 2027 (Gartner). 69% of AI projects do not reach live operational use (Blue Prism). Developer momentum metrics are not revenue metrics.

Regulatory uncertainty (medium). EU AI Act enforcement begins August 2026. How autonomous purchasing agents are classified under existing consumer protection and financial regulation frameworks is unresolved. Compliance costs could make small-scale agent operations economically unviable.

7. Three Phases, One Bet: Structural Inevitability

Near-term (2026): Consumer agent shopping scales through OpenAI, Google, and Shopify integrations. Payment rails begin consolidating around 2–3 dominant standards. Forrester predicts 1 in 5 B2B sellers will face agent-led quote negotiations this year. Enterprise pilots increase; most fail. Answer Engine Optimization emerges as a real discipline and agent legibility of merchant product data becomes a competitive variable.

Mid-term (2027–2028): Agent-to-agent commerce reaches meaningful volume. Micropayments become the default billing model for agent API access. Privacy and identity layers mature to handle regulated enterprise use cases. B2B moves faster than expected: agent-led quote negotiations reach 20% of B2B sellers by 2026 (Forrester), with agent-to-agent procurement becoming the highest-volume micropayment category by 2028.

Long-term (2029–2030): Agents manage budgets, execute multi-step procurement, and negotiate contracts autonomously. The operational distinction between e-commerce and agentic commerce collapses.

So What?

The structural thesis for agentic commerce is high conviction. The timing thesis is low conviction. The infrastructure being built today, wallets, rails, execution environments, identity, underpins both the bull and bear scenario. The question is not whether demand arrives but is how much runway builders have before it does.

MagicBlock Research. MagicBlock builds Ephemeral Rollup infrastructure on Solana, providing private, fast, elastic and low-cost execution for onchain applications.

Sources: McKinsey (Oct 2025), Bain & Company (Nov 2025), Morgan Stanley (Dec 2025), Gartner (Nov 2025), IDC (2025), Adobe, Salesforce, Coinbase, Stripe, OpenAI, Google Cloud Blog, Forrester, Blue Prism Global Enterprise AI Survey (2025), McKinsey/Artemis, US Treasury, HKMA, European Commission.