.jpg)

Key Takeaways

- The global FX market trades $7.5T a day. EDXM's April 2026 launch of KRW/USD perpetuals (Citadel Securities, Fidelity, Virtu, integrated into Spark Systems) confirms that stablecoin-settled FX derivatives are a real product for institutional participants.

- Every synthetic FX project to date has failed: Synthetix sEUR, Handle.fi, Nabla. The failures were structural, and the common thread is the same: supply without demand. Any new FX venue has to address this explicitly.

- 99% of stablecoin supply is USD-denominated. EURC sits at ~$420M and has contracted from its late-2025 peak. Multi-currency spot FX is a three-to-five-year bet. Oracle-priced perpetuals settled in USDC are the only model that makes structural sense in the current environment.

- Solana has the infrastructure: $17B+ in stablecoins, ~$1.6B in daily perp volume in 2025, Pyth feeds on every major pair. Flash Trade and GMTrade have listed FX and scaled to under $30M combined daily. The bottleneck doesn't appear to be strictly technical. Yet no one has built FX-grade microstructure to offer infrastructure FX market makers can actually use to attract institutional-grade liquidity.

Primer

The traditional foreign exchange market processes approximately $7.5 trillion in daily volume, making it the largest financial market on earth. It is not a single market but an ecosystem of distinct participants, each transacting for fundamentally different reasons:

- Multinational corporations engage in FX daily to manage treasury operations, converting revenues earned abroad back into their home currency and hedging future cash flows against exchange rate volatility.

- Import/export businesses need settlement currency for every cross-border shipment, converting between currencies on each invoice. Smaller merchants are often hit hardest by FX spreads, lacking the volume to negotiate institutional rates.

- Banks and dealer desks sit at the center of the system: they facilitate client orders, warehouse risk, and offset positions in the interbank market. The top 10 dealer banks handle roughly 75% of all FX volume.

- Central banks participate through foreign reserve management and periodic market interventions to stabilize or influence their domestic currency.

- Institutional investors and asset managers generate FX flows as a byproduct of cross-border portfolio allocation. Every purchase of a foreign equity or bond creates a currency obligation that must be hedged or left open.

- Remittance companies (Wise, Western Union, Remitly) process billions in migrant worker transfers across high-volume, small-ticket corridors where the FX spread is the primary revenue driver.

- Insurance and reinsurance companies with global claims obligations require multi-currency liquidity to pay out across jurisdictions, often on short notice following catastrophic events.

- Sovereign wealth funds managing national reserves across currencies contribute ongoing rebalancing flows, typically executed discreetly through custodian banks.

What unites all of these participants is that most are not trading FX speculatively, they are compelled to transact by underlying business needs. The market's $7.5 trillion daily volume is overwhelmingly driven by hedging, settlement, and portfolio management rather than directional bets on currency movements.

Despite the rapid maturation of decentralized finance infrastructure, onchain forex remains a nearly untouched frontier. This report focuses specifically on the trading and price discovery layer: the infrastructure through which FX transactions are executed, matched, and settled. While the broader payment and remittance use cases for stablecoins are significant and growing, this research piece examines whether blockchain infrastructure, and Solana in particular, can serve as a viable venue for FX execution through spot conversion and leveraged derivatives.

Section 1: Types of Onchain Forex

Onchain forex activity today falls into four distinct categories, each with different levels of maturity, liquidity, and market traction. Understanding these categories is essential for identifying where genuine opportunity exists versus where the market has already attempted and failed.

1.1 Stablecoin Spot Swaps

The most common form of onchain FX is stablecoin-to-stablecoin swaps on decentralized exchanges. When a user swaps USDC for EURC on Jupiter or Uniswap, they are performing a de facto foreign exchange transaction. However, this activity is overwhelmingly driven by payment and treasury use cases rather than speculative FX trading.

EURC (Circle's euro stablecoin) trades approximately $57M in daily volume across all venues, with a market cap of ~$460M. On Solana, EURC is available through Jupiter and is supported as collateral on Jupiter Lend, but onchain liquidity depth remains thin. A trade of $500K+ in EURC/USDC would produce meaningful slippage on most venues. For context: traditional EUR/USD trades $2.3 trillion daily. Current onchain EUR/USD equivalent volume represents approximately 0.002% of the traditional market.

1.2 Oracle-Priced Perpetual Futures

Perpetual futures settled in USDC but priced against FX oracle feeds allow traders to gain exposure to currency movements without either party needing to hold the underlying fiat stablecoin. Settlement is in USDC, and pricing is derived from oracle feeds (e.g., Pyth, which already provides real-time feeds for all major FX pairs on Solana). The key advantage of this model is that it sidesteps the non-USD stablecoin liquidity problem entirely: no EURC, JPYC, or other fiat stablecoins are required on either side of the trade.

On Solana, a small number of protocols have begun listing FX pairs. Flash Trade, a decentralized perpetual exchange using a pool-to-peer liquidity model, offers forex and metals perpetuals alongside its crypto markets with up to 20x leverage and zero-slippage execution via Pyth oracles. GMTrade launched forex perpetuals on Solana in January 2026, supporting GBP/USD, EUR/USD, AUD/USD, and NZD/USD using an AMM model. However, neither has achieved meaningful FX-specific volume relative to their crypto markets.

Outside Solana, the most notable institutional attempt is EDXM International (backed by Citadel Securities, Fidelity Digital Assets, and Charles Schwab), which announced a blockchain-based KRW/USD perpetual targeting $500M in average daily volume within its first year.

1.3 Synthetic FX Tokens

Several protocols have attempted to create synthetic representations of fiat currencies onchain. The most established example is Synthetix on Ethereum/Optimism, which supports forex synths including sEUR, sJPY, sKRW, and sAUD. Users mint synths by staking the protocol's native SNX token at a 650%+ collateralization ratio, meaning $650 in SNX must be locked to create $100 of synthetic currency. FX trading carried a 5 basis point fee with zero slippage regardless of size, since all trades settle against a pooled debt model. At its peak, sEUR accounted for roughly 10% of Synthetix mainnet transactions. However, forex has remained a minor vertical. Crypto perps dominate usage, and forex synth liquidity contracted significantly in the last 3 years.

Handle.fi offered minted fxTokens (fxEUR, fxJPY, fxGBP) collateralized by crypto assets. Nabla on Pendulum built a forex-optimized AMM targeting underserved corridors like BRL and TZS. Neither gained meaningful traction.

On Solana, no protocol has attempted the synthetic FX token model. This is likely because Solana's DeFi ecosystem has evolved around a different philosophy: rather than creating synthetic representations of assets, Solana protocols have favored direct asset trading (spot DEXs like Jupiter) and oracle-priced derivatives (perp platforms like Drift and Flash Trade).

The synthetic model faces a fundamental problem: without sufficient demand, there is no incentive to hold the collateral to facilitate the synthetic swaps. Compared to EURC, for example, a synthetic fxEUR has worse capital efficiency (over-collateralized vs. 1:1 backed), worse composability (fragmented across protocols), additional risk (collateral liquidation, debt pool dynamics, peg mechanism complexity) with no compensating benefit or yield advantage that couldn't be replicated by holding EURC in a lending market.

1.4 Institutional Settlement Rails

A separate category is the use of blockchain rails for institutional FX settlement. HSBC has settled approximately $2.5 trillion in bilateral FX trades using Baton Systems' distributed ledger technology. JP Morgan's Onyx platform processes cross-border payments using tokenized deposits. These are permissioned, private blockchain implementations and are not directly accessible to DeFi participants, but they validate the thesis that a “cheap ledger” infrastructure improves FX settlement.

Section 2: Market Size

2.1 Traditional FX Market

The global foreign exchange market trades approximately $7.5 trillion per day, making it the largest and most liquid financial market in the world. The market is dominated by a small number of major currency pairs, with EUR/USD alone accounting for roughly $2.3 trillion in daily volume. The non-deliverable forward (NDF) segment, which covers restricted currencies like KRW, BRL, INR, and TWD, processes approximately $2.5 trillion daily and represents the most compelling target for onchain disruption.

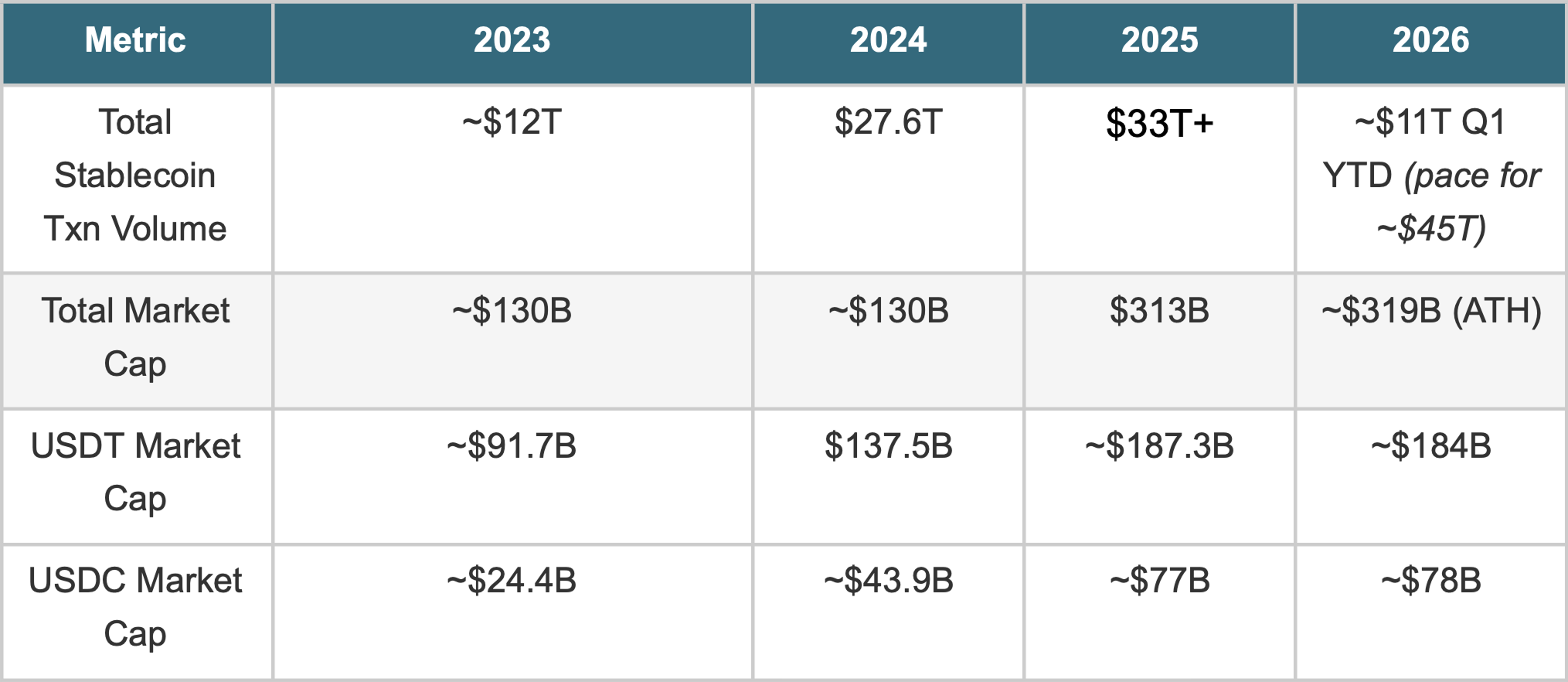

2.2 Stablecoin Market

The stablecoin market has grown into critical financial infrastructure. Total stablecoin transaction volume exceeded $33 trillion in 2025, up from $27.6 trillion in 2024. The total market capitalization reached an all-time high of approximately $319 billion in April 2026, representing more than 50% growth since early 2025.

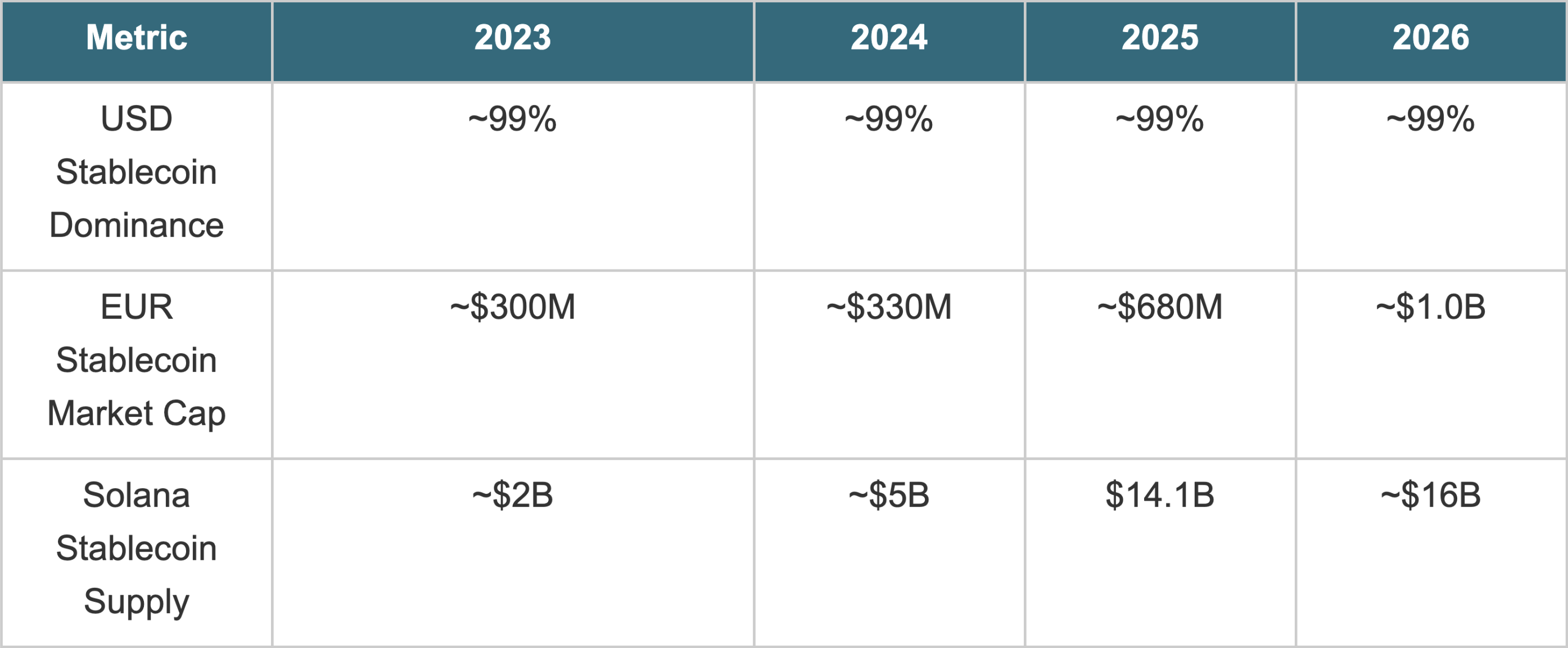

USD stablecoins dominate at 99% of the market. The entire euro stablecoin ecosystem ($680M) is smaller than a single mid-cap altcoin. JPY stablecoins only received regulatory approval in August 2025, with the first yen-pegged stablecoin launching in October 2025. GBP, CHF, AUD, and SGD stablecoins are effectively non-existent at scale. This means any onchain FX venue requiring non-USD stablecoins on both sides of the pair faces an immediate liquidity desert.

2.3 EURC: The Non-USD Stablecoin Leader

Circle's EURC is the largest non-USD stablecoin, with a market cap of approximately $420M and daily trading volume around $30–60M (varying significantly day to day). Growth was initially driven by MiCA regulatory clarity in the EU, which reversed a 48% contraction in euro stablecoin market cap that occurred in the year before MiCA implementation. However, EURC's market cap has retreated from a peak near $460M in late 2025 to ~$420M in April 2026, with circulating supply declining from 396M to approximately 360M tokens, a sign that adoption remains uneven and usage is still heavily influenced by short-term trading cycles rather than sustained commercial demand.

- Post-MiCA growth: Euro stablecoin market cap doubled in the 12 months after MiCA's June 2024 rollout

- Volume surge: Monthly euro stablecoin transaction volume rose nearly 9x to $3.83B after MiCA

- EURC volume growth: EURC trading volumes expanded 1,139% post-MiCA

- Solana traction: The number of independent non-USD stablecoin senders on Solana has grown nearly 3x year over year, driven mainly by EURC and the Brazilian real stablecoin BRZ

Despite the post-MiCA momentum, EURC's market cap remains less than 0.15% of USD stablecoin market cap, and its daily volume would fill a single minute of traditional EUR/USD trading. The European banking sector is beginning to respond: a consortium of 12 European banks is reportedly working to put the euro onchain to compete with dollar dominance in crypto markets, a development that could either accelerate EURC adoption or fragment the euro stablecoin market further.

2.4 Perp DEX Market

Decentralized perpetual futures exchanges have become the fastest-growing vertical in DeFi and are now a structurally significant share of global derivatives. Perpetual DEXs command approximately 26% of the crypto-derivatives market, up from single digits just a year ago and roughly 1% in 2022. Total daily perp DEX volume regularly exceeds $20 billion, with $22.6 billion recorded in a recent 24-hour period across all platforms.

Hyperliquid dominates with roughly 38–44% of all perp DEX volume, having processed over $2.76 trillion in cumulative volume. Daily volumes on Hyperliquid alone regularly exceed $15 billion, with peaks above $29 billion. Aster, edgeX, and Lighter compete for remaining share. None of these platforms currently list FX pairs, though Hyperliquid's HIP-3 framework for permissionless perpetual markets has enabled commodity contracts (including oil and silver futures), suggesting FX could follow.

On Solana specifically, the perp ecosystem is deep and competitive. Jupiter processed $264 billion in perp volume in 2025. Drift Protocol handled $92 billion in 2025 perp volume with 40+ markets and up to 101x leverage. However, Drift suffered a catastrophic $270–285 million exploit in early April 2026, the result of a six-month social engineering operation by North Korean state-affiliated hackers, which has significantly shaken confidence in the protocol. Pacifica, a new entrant founded by former FTX COO Constance Wang, has at times surpassed both Jupiter and Drift in daily volumes despite being in beta.

Despite this mature and high-volume infrastructure, FX pairs remain almost entirely absent from Solana's perp landscape. The only exceptions are platforms like Flash Trade and GMTrade (which launched EUR/USD, GBP/USD, AUD/USD, and NZD/USD perpetuals in January 2026), neither of which has attracted volume comparable to their crypto markets.

Section 3: Opportunities

3.1 The Infrastructure-Demand Gap

The most striking observation is the disconnect between infrastructure readiness and market development. Solana processes $1B+ in daily DEX volume and hosts $17B in stablecoins with the highest velocity of any major chain: every stablecoin dollar on Solana turns over six times faster than on Ethereum. Pyth Network provides real-time FX oracle feeds for all major currency pairs. The protocols that have listed FX (Flash Trade, GMTrade) have proven the technical viability, but volume remains marginal. Meanwhile, EDXM's April 2026 launch of KRW/USD perpetuals validates that there is real institutional demand for onchain FX derivatives.

3.2 propAMM: Enabling Institutional-Grade FX Quoting

The central obstacle for onchain FX is not just listing pairs, but achieving the spread tightness and execution quality that FX participants demand. Traditional FX major pairs trade at spreads of 0.5 to 2 basis points. Even the most liquid crypto AMMs offer spreads 50x wider. This is a market microstructure problem and a propAMM can give the market maker active control over their quoting strategy while retaining the onchain settlement and composability benefits of an AMM architecture. The market maker provides liquidity and can:

- Quote around the oracle price with custom spreads: setting tight spreads during liquid, low-volatility conditions and widening them during economic data releases, central bank interventions, or periods of toxic flow, exactly as they would on a traditional eFX platform.

- Manage inventory proactively: adjusting their positioning based on accumulated flow rather than being passively arbitraged into an unfavorable inventory position.

- Respond to market events in real time: pulling quotes or shifting spreads within milliseconds.

- Compete on execution quality: multiple market makers can quote on the same propAMM venue, with traders receiving the tightest available spread through competition, mirroring the multi-dealer model that dominates institutional FX (platforms like FXall, 360T, and Spark Systems).

In traditional FX, a market maker's edge comes from their ability to price risk intelligently: reading flow, managing inventory, adjusting for volatility, and quoting tighter than competitors. One promising avenue to achieve competitiveness for market makers with this kind of set up is through Ephemeral Rollups (ERs). ERs are dedicated execution environments that can mirror the performance of offchain infrastructure while maintaining the verifiability and liquidity of Solana. ERs offer:

- Real-time execution speed: ERs process transactions in real-time and enable quote updates to execute predictably

- Gasless transactions: Eliminates the UX friction and cost unpredictability that deters traditional FX participants

- Compliance: ER nodes can be colocated and configured to meet jurisdiction-specific compliance requirements or only allow a whitelisted set of participants to trade

- Privacy: Offer confidential execution, addressing the order flow privacy requirements that are critical for some institutional FX participants.

The combination of real-time and predictable execution, gasless transactions, compliance and private order flow creates a trading environment that no existing DEX can replicate. For FX market makers accustomed to the performance and privacy of traditional venues, this constitutes a viable infrastructure for institutional FX liquidity to migrate onchain.

3.3 The Opportunity Ahead

The convergence of mature onchain infrastructure, regulatory clarity (MiCA, GENIUS Act), and institutional validation (EDXM's KRW/USD launch) creates a window of opportunity that is unlikely to remain open indefinitely. Traditional FX platforms are exploring blockchain settlement. The next 12–24 months will likely determine which execution layer captures the foundation of onchain FX and the first movers who solve the liquidity bootstrapping problem will benefit from the same network effects that made Uniswap the default for spot crypto and Hyperliquid the default for perps.

The opportunity unfolds across three horizons:

Near-term (0–6 months): Restricted currency perpetuals

EDXM has validated institutional demand for onchain NDF alternatives with its KRW/USD product. But EDXM is a single venue targeting a single pair through a centralized exchange model. The remaining restricted currency universe (BRL, INR, TWD, PHP etc.) is wide open for new entrants. A startup launching oracle-priced perpetuals for 2–3 restricted currency pairs and/or a propAMM with Ephemeral Rollups can capture first-mover positioning in corridors where the traditional spread (3–10+ basis points) gives ample room to offer a competitive product. The PER privacy guarantee and permissioned access provides a concrete value proposition for onboarding the first 3–5 market makers. This phase is about proving execution quality and building a track record. $10–50M daily volume would represent meaningful proof of concept and put the venue on the radar of institutional FX desks.

Medium-term (6–12 months): G10 FX pairs and spot stablecoin FX

Once execution quality and market maker relationships are proven on restricted currencies, the venue can expand to major G10 pairs (EUR/USD, GBP/USD, USD/JPY). These corridors are more competitive, spreads are tighter and incumbents are deeply entrenched, but the 24/7 availability, reduced counterparty risk, and onchain settlement offer genuine differentiation for segments that are underserved by traditional FX infrastructure (crypto-native treasuries, DeFi protocols with multi-currency exposure, weekend and off-hours hedging). Simultaneously, as EURC and other non-USD stablecoins mature under MiCA and equivalent frameworks, spot stablecoin FX trading (USDC/EURC) becomes viable as a parallel product line. Integrating with institutional eFX platforms and allowing traditional FX desks to access onchain liquidity through familiar interfaces is key to bridging the divide.

Long-term (12–24 months): The onchain FX venue

The endgame is a full-spectrum FX venue on Solana: spot stablecoin swaps, perpetual futures across G10 and restricted currencies, and eventually forwards and options. As non-USD stablecoins mature (JPY, GBP, CHF stablecoins following the path EURC has pioneered), the addressable market expands from derivative exposure to actual cross-currency settlement. Corporate treasury, cross-border payments, and remittance flows begin routing through the venue because onchain settlement is faster, cheaper, and more transparent than the correspondent banking system it replaces.

The builders who capture this opportunity will build the execution layer through which a meaningful share of the world's largest financial market eventually routes. The tools exist. The regulatory frameworks are crystallizing. The institutional demand is validated. What remains is execution.