.jpg)

Disclosure

This piece is written by an operator with positions in both narratives. The author leads BD at MagicBlock and is a TCG fanatic. The analysis should be read in light of these positions. The underlying data is independently sourced.

Key Takeaways

1. Pokemon TCG Pocket made $990 million in 2025 selling digital packs that cannot be traded. Whatnot did $8B GMV with sports and trading cards as its top two US categories. Pop Mart did $1.8B from blind boxes. In mass-market collectibles, people pay for the thrill of opening a pack, not for the card itself. Trading happens after.

2. Every pure-digital NFT collectibles project has either collapsed or plateaued. NBA Top Shot fell 99% from its $226M monthly peak. Topps NFT is shutting down March 31, 2025. Sorare is a real $50M revenue business but sits roughly 30x below the original peak expectations that supported a $4.3B valuation. The structural issue was not the entertainment layer. It was the absence of a durable underlying asset combined with weaker IP than the next wave inherits.

3. Physical-backed onchain is working. Collector Crypt and Phygitals combined hit $20M weekly trading volume on Solana in September 2025, surpassing regular Solana NFT trading that week. Courtyard raised $30M from Y Combinator, ParaFi, and NEA. Physical-backed plus gacha-led is the only onchain collectibles model currently showing breakout growth in this category.

4. The bottleneck for the next 10x is standardized trust infrastructure. The historical analogy is PSA, the grading company that standardized authentication on physical cards and built itself into a $700M+ business in the process. Verifiable randomness is the analogous trust primitive for onchain gacha. The market is moving from trusted sellers to verifiable proofs.

Primer

The collectibles market is not a marketplace problem. It is an entertainment problem.

Pokemon Company produced 10.2 billion cards in 2024–2025, and the retail product is a sealed booster pack. The consumer experience is the thrill of the pull. The secondary trading market is a downstream phenomenon, it exists only because the dopamine rush of opening the pack came first.

For decades this loop scaled thanks to an established trust model. You bought packs from a sealed retail supplier, you graded valuable cards through PSA, you traded with people you trusted at your local card shop. The whole industry ran on trusted parties and physical chains of custody.

Live commerce shifted the loop to streamers. Whatnot generated $8B in GMV in 2025, doubling year over year, with sports and trading cards as its top two categories. The breaker on camera became the new trust anchor. You buy a pack ripped on a livestream because you trust the seller is opening it honestly.

That trust model is now under sustained legal and reputational pressure. Whatnot is facing 15 arbitration claims and illegal gambling allegations. Major breakers including Backyard Breaks and Platinum Card Breaks have been accused of shill bidding, leaking pack contents to favored buyers via direct messages, and faking pulls. The breaker economy works only because users trust the operator. The strength of that trust is no longer assured.

The same thing happened to physical cards before PSA. Every transaction needed individual due diligence. The market could not scale until someone built a portable, standardized credential that meant: this card is real, this is its condition. PSA built that credential and the card market exploded around it.

Now that data shows the next wave of collectibles is moving onchain, we think it wins for the same structural reason, this time replacing trusted sellers with verifiable proofs. Verifiable randomness for pack openings, onchain custody for redemption, composable secondary markets are all part of a technology stack that ultimately provides more guarantees to the market.

Onchain collectibles win where randomness, custody, redemption, and secondary liquidity can happen in real time without trust assumption. The rest of this piece is an argument for why these properties are the wedge to expand the collectible market onchain.

Section 1: Types of Onchain Collectibles Activity

Onchain collectibles activity today falls into four categories with very different maturity and traction.

1.1 Tokenized Physical Cards

This is the segment currently demonstrating sustained market traction. Real cards are vaulted, tokenized as NFTs, and traded onchain. Physical redemption is available. The pack-opening experience drives initial mint and secondary trading takes place from there.

Collector Crypt on Solana went from $44M in monthly volume in August 2025 to $165M by April 2026. Its CARDS token launched in late August 2025 and gained 2,400% in two weeks. The platform has tokenized over 130,000 physical Pokemon cards.

Phygitals on Solana runs a similar model with a different angle. Users open digital packs that reveal a physical card. They can keep the digital token, redeem the physical card, or sell back to the platform for 85% of market value. Phygitals splits the Solana TCG segment roughly evenly with Collector Crypt in tracked weekly volume, but with materially more active wallets (around 14K vs. roughly 4K). More users at smaller per-user spend.

Courtyard on Polygon is the largest of the three by single-month volume. It generated $78M in Pokemon NFT secondary sales in August 2025, its best month ever. It has brought over 500,000 physical collectibles onchain, and minted over 3 million trading cards as NFTs.

Combined, Solana TCG NFTs surpassed regular Solana NFT trading volume at $20M per week in September 2025. This is the only onchain collectibles segment with a real growth curve vs traditional NFT.

1.2 Pure-Digital NFT Collectibles

This is the segment that has consistently failed to convert speculative interest into durable demand.

NBA Top Shot peaked at $226M in monthly volume in February 2021. By early 2025 it was under $2M per month, a 99% decline. The structural issue was that financial speculation outran fan engagement, supply exploded faster than demand and no utility remained once the speculative cycle ended.

Topps NFT migrated from WAX to Avalanche in 2021 with strong IP backing including MLB, F1, Bundesliga, and UEFA. It announced in early 2025 that its marketplace would close on March 31, 2025, citing years of marketplace errors and very little uptime. Topps lost its 70-year MLB licensing deal to Fanatics in 2021 and pulled out of its planned SPAC merger shortly after.

Sorare is the most nuanced of the failures. Revenue went from $167M in 2022 to $69M in 2023 to $50M in 2024. EBITDA losses halved in 2024 to $117M. Monthly transaction count hit an all-time high in August 2025. The platform has real licensing deals with the Premier League, NBA, MLB, MLS, and NBPA. Sorare is a durable business at $50M of annual revenue. It is roughly 30x below the original peak expectations that supported a $4.3B valuation. The product is real but it has plateaued at a niche.

The common thread is that digital scarcity alone did not create defensible demand. Without strong IP or physical backing, the proposition collapsed once the speculative cycle ended.

1.3 Fractionalization

Fractionalization platforms tried to make illiquid collectibles tradeable by selling shares of high-value items. The category has largely failed to sustain product-market fit.

Otis was acquired by Public.com in March 2022. Public liquidated most of the platform's assets afterward. Mythic Markets closed and sold its assets to Heritage Auctions. Collectable was acquired and its assets are reportedly held hostage by the new owners. Rally remains operational but Sports Illustrated has called sports-card fractional investing a failure for most investors.

Structural failure can be traced back to regulatory complexity around Reg A offerings, thin secondary liquidity, no compelling reason to fractionalize assets that are not appreciating fast enough to justify the friction.

1.4 Onchain Gacha and Pack Opening

This is the most underbuilt category of the four, and the one the next wave is starting to occupy.

Magic Eden partnered with Collector Crypt to launch RWA Pokemon pack drops in 2025. Phygitals' core experience is exactly this: a digital pack reveal that maps to a physical card. Collector Crypt's $165M monthly volume in April 2026 is largely driven by gacha mechanics, not pure secondary trading.

But public materials rarely foreground verifiable randomness as a first-class trust primitive for these pulls. Most onchain pack openings today still rely largely on the platform's word that the randomness is fair. This is the same kind of trust standardization PSA introduced for physical cards, and the role VRF can play for digital pulls.

Section 2: Market Size

Sizing this market requires analyzing separately three layers: traditional collectible, probability-based entertainment and the onchain market. The traditional collectible market is large but mature. The thrill-seeking, probabilistic entertainment layer that sits with live commerce and gacha is much larger. The onchain wedge today is still rounding error against either, but growing fast.

2.1 The Traditional Collectibles Market

Sports trading cards run $1.8 to $2B annually for the narrow market, $6.7B for the broader Panini-style segment. Fanatics Collectibles generated $1.6B in revenue in 2024, up 40% year over year, with EBITDA margins above 20%. Sneaker resale in the US hit $6B in 2025 and is projected to reach $51.2B by 2032. Global luxury watches at retail are a $46-47B market. Sports memorabilia is $26-38B depending on the source.

Pokemon TCG global retail sales topped $2B in 2024, in a year when card unit production fell roughly 14% from the prior fiscal year's record 11.9 billion. Bandai Namco's Toys & Hobby segment, where its TCG business sits, generated roughly $3.4B in fiscal 2024 with capsule toys and cards as the major contributors. Japan alone bought $857M of Pokemon TCG products in fiscal April 2023 to March 2024, more than the next eight TCGs combined including Yu-Gi-Oh, Magic the Gathering, and One Piece.

These are the headline numbers crypto research usually anchors on. They are not where the interesting volume is.

2.2 Probability as the Demand Engine

The dopamine-seeking consumer behavior is the real opportunity

Pokemon TCG Pocket launched October 2024. By the end of 2025 it had generated $1.49 billion in lifetime revenue against 100 million downloads, making it the highest-grossing mobile card battler in history. In 2025 alone it earned $990M, the third-highest IP-based mobile title behind only Monopoly Go and Honor of Kings, ahead of Pokemon Go and Call of Duty Mobile.

Pop Mart did $1.8B in revenue in 2024, up 107% year over year. In the first half of 2025 alone the company generated $1.95B in revenue, up 204% year over year, exceeding its entire 2024. Pop Mart's Labubu IP alone contributed 34.7% of H1 2025 revenue, up 668% year over year. The global capsule toy and blind-box market is projected to surpass $20B in 2025, up from $15.9B in 2024.

Whatnot does $8B in GMV at an $11.5B valuation, with sports and TCG as its top two categories, 6.4M sports cards sold per month, two cards sold every second globally. Users spend 95 minutes per day on the platform on average.

Live commerce more broadly is multi-trillion-dollar at the global level. TikTok Shop did $66B in GMV in 2025 with live commerce roughly 14% of that, around $9.2B. China's Douyin e-commerce GMV was $487B in 2024 with live commerce at 40-58%, around $195-280B. Not all of this is collectibles. The relevant point is the consumer behavior, not the addressable market. Probabilistic and live commerce sit inside a multi-trillion-dollar behavior stack. The collectibles slice is a few percent. That slice alone is multi-billions.

2.3 Onchain Today

Solana's overall NFT marketplace volume grew 45% in Q3 2025. Collector Crypt processed $165M in April 2026. Phygitals scaled to 14K+ active wallets with weekly gacha volume growing 10x in a single September week.

The active player landscape spans multiple chains and product approaches. On Solana, Collector Crypt focuses on pack rips of graded Pokemon cards (130K+ tokenized, $165M monthly volume). Phygitals pairs digital pack reveals with physical card delivery and launched a storefront on Fanatics Collect in April 2026, a notable Web3-to-Web2 integration. Emporium runs a claw-machine gacha format on Solana. Courtyard, on Polygon with Brink's-vaulted inventory and a zero-fee marketplace, has tokenized over 100,000 cards across $200M+ in volume. Smaller entrants include RIP.FUN on Base as a tracking and aggregation layer, Beezie on Flow (Now also on Solana), and Drip on Ronin. Magic Eden anchors much of the distribution layer with partnerships across these platforms. The competitive set is fragmented today with no clear winner across chains.

These are real numbers but still small against $8B Whatnot GMV. The thesis is not that onchain replaces Whatnot at the platform level. It is that onchain captures the share of activity where trust, custody, redemption, and secondary composability matter most, and that this share expands as the underlying infrastructure matures.

Section 3: Opportunities

3.1 Asia as the Proof Market

Most crypto research treats collectibles as a US story. The actual gravity sits in Asia.

Japan's domestic gachapon market did roughly $540M in fiscal 2024, up 23% year over year. It is projected to cross $670M in 2025. Bandai Namco holds 56% of the Japanese capsule toy market and releases over 100 new SKUs per month. There are 312 dedicated Gashapon Department Stores and GBO Shops nationwide. Japan normalized probabilistic consumer commerce decades before crypto existed. Capsule toys date to the 1960s, gachapon vending to the 1990s, kuji lottery merchandise to the 2000s. Verifiable randomness is not a foreign concept for this audience. It is a natural digitization of behavior they already do.

The same dynamic exists in K-pop. The four major Korean entertainment companies generated $590M in merchandise revenue in 2024, projected to cross $745M in 2025. Photocards are the largest single category. International physical album sales hit $291.8M in 2024. The Korean secondary resale platform Bunjang, where K-pop accounts for roughly 70% of international transactions, is valued at $520M.

The K-pop photocard model is gacha-native by design. Album buyers do not know which photocard they will get. Randomized Pre-Order Benefits and Lucky Draw cards have expanded dramatically over the last five years, with major 2026 releases now reportedly running into the high teens of retailer-exclusive variants per member. Fans trade on Twitter, Mercari, Depop, and Carousell. AI-based condition grading apps have grown into a meaningful share of K-pop card authentication, mirroring the role PSA played for sports cards a decade earlier. The demographic is younger, mobile-native, and culturally bought in to digital identity. This is one of the most structurally compatible audiences in the entire collectibles space for onchain coordination, and almost no Web3 project is targeting it directly.

3.2 Where the Market Expands From Here

Onchain TCG is at roughly $20M per week in trading volume and growing 27% week over week, while the surrounding traditional gacha economy operates at orders of magnitude greater scale. The gap is not a sign the market is broken. Trusted platforms are generating real revenue today, and consumers are paying without onchain guarantees. The opportunity is to expand the market the way PSA grading did for physical cards.

PSA grading, which expanded the addressable card market by an order of magnitude. The same kind of expansion is available here, with different new participants: cross-border collectors, lending and LP markets, agent-driven micro-buyers, and fractional exposure traders. What is missing is the product layer that puts the infrastructure to work.

3.3 The Trust Primitive: PSA Then, VRF Now

The analogy is structurally similar, though applied at a different point in the product lifecycle. PSA verifies asset quality after creation. VRF verifies allocation fairness before reveal. Same trust-layer function in market structure, different moment of intervention.

Pre-PSA, the physical card market had a trust problem identical in shape to the breaker economy today. Was this 1986 Donruss Bonds in near-mint condition or very good? Was it doctored? Was it real? Every transaction needed individual due diligence and personal relationships. The market could not scale to institutional capital until someone standardized the credential.

PSA built that credential. A PSA 10 Charizard trades anywhere in the world without inspection because the grade is portable, verifiable, and trusted. Standardized trust created fungibility, which created liquidity, which created the modern card market. PSA itself became a $700-850M business as a byproduct of providing the trust primitive.

Verifiable randomness is the analogous primitive for the allocation layer of onchain pack openings. Today a Whatnot breaker opening packs on camera asks viewers to trust three things: that the packs are sealed, that the breaker is not stacking or skimming, and that the algorithmic assignment of pack to buyer is honest. VRF solves only the third. The other two require vaulted inventory with public commitments and verifiable redemption guarantees. The full trust stack is VRF for randomness, onchain custody for inventory, and onchain title for redemption. With that stack, an onchain pack opening removes operator discretion from the allocation layer, creates auditable allocation records, and meaningfully reduces the kinds of discretionary manipulation that have driven the breaker industry's current trust crisis.

3.4 Why Crypto (Not Just Centralized Provably-Fair RNG)

A skeptical reader has an obvious counter. Crypto casinos have marketed "provably fair" systems for years, but most still rely on offchain logic, custodial balances, or centralized servers. True onchain implementations remained niche. The more relevant point is that trusted versions of these markets already have product-market fit. Most online gambling users still pick centralized brand-name platforms like DraftKings and FanDuel rather than verifiable alternatives. If fairness alone were enough to win consumers, the verifiable category would already dominate. It does not.

The honest answer: fairness alone is not the differentiator. Three structural advantages are.

Multi-party coordination. The modern collectibles economy involves IP licensors (Pokemon Company, MLB, K-pop labels), card manufacturers, vault custodians, graders (PSA, BGS, SGC), marketplaces (eBay, TCGPlayer, Whatnot, Mercari), live commerce platforms, individual breakers, and liquidity providers. Today these are coordinated through bilateral contracts and siloed databases. Onchain rails collapse the coordination layer into shared composable state. No platform has to own all the relationships.

Secondary composability. A pulled card on Whatnot is just a card. A pulled card onchain is also collateral, tournament entry, lending inventory, LP inventory, or fractionalized exposure. Web2 stacks require custom integration for every adjacent product. Onchain is permissionlessly composable by default.

Global 24/7 liquidity. Collectibles markets are already borderless. Pokemon Japan cards trade in Hong Kong, K-pop photocards trade between Korea and Brazil, Charizards trade between Tokyo and New York. The traditional rails for cross-border collectible commerce are bad: bank transfers, FX spreads, payment processor disputes, settlement delays. Crypto rails are 24/7, stablecoin-settled, and structurally lower-trust by default.

Provable fairness alone did not win casino users. Fairness plus coordination plus composability is a different bundle, and collectibles are the first consumer category where all three matter simultaneously.

3.5 The Stack Required

The product layer needs three primitives working together: verifiable randomness for the allocation moment, low-latency execution for the live-stream-fast UX consumers expect, and onchain custody and title for the vaulted physical inventory. The first two are the gating constraints today.

MagicBlock is one implementation of this stack: audited VRF, low-latency execution through Ephemeral Rollups, and Solana-native settlement. Its VRF service is free when called from Ephemeral Rollups, and pack-opening UX on Ephemeral Rollups runs in the sub-50ms range. This is the latency window in which live multi-buyer pack auctions, pooled breaks, and asynchronous redemption flows become practical onchain rather than offchain.

A concrete picture. A Korean entertainment label drops a new album with limited-edition photocard variants. Fifty fans join a live pack-opening stream. Each digital pack is backed by a physical photocard sitting in a vetted vault, with the inventory commitment posted onchain. Verifiable randomness assigns the random pack-to-buyer mapping with cryptographic proof. The reveal happens in real time. Rare pulls auto-list to a secondary marketplace during the stream. A fan in São Paulo who pulls a rare card can redeem the physical via vault shipping, hold the token and trade later, or use it as collateral in a lending pool. Every step is auditable on Solana. This is the workflow that becomes economical for the first time when the three primitives are combined.

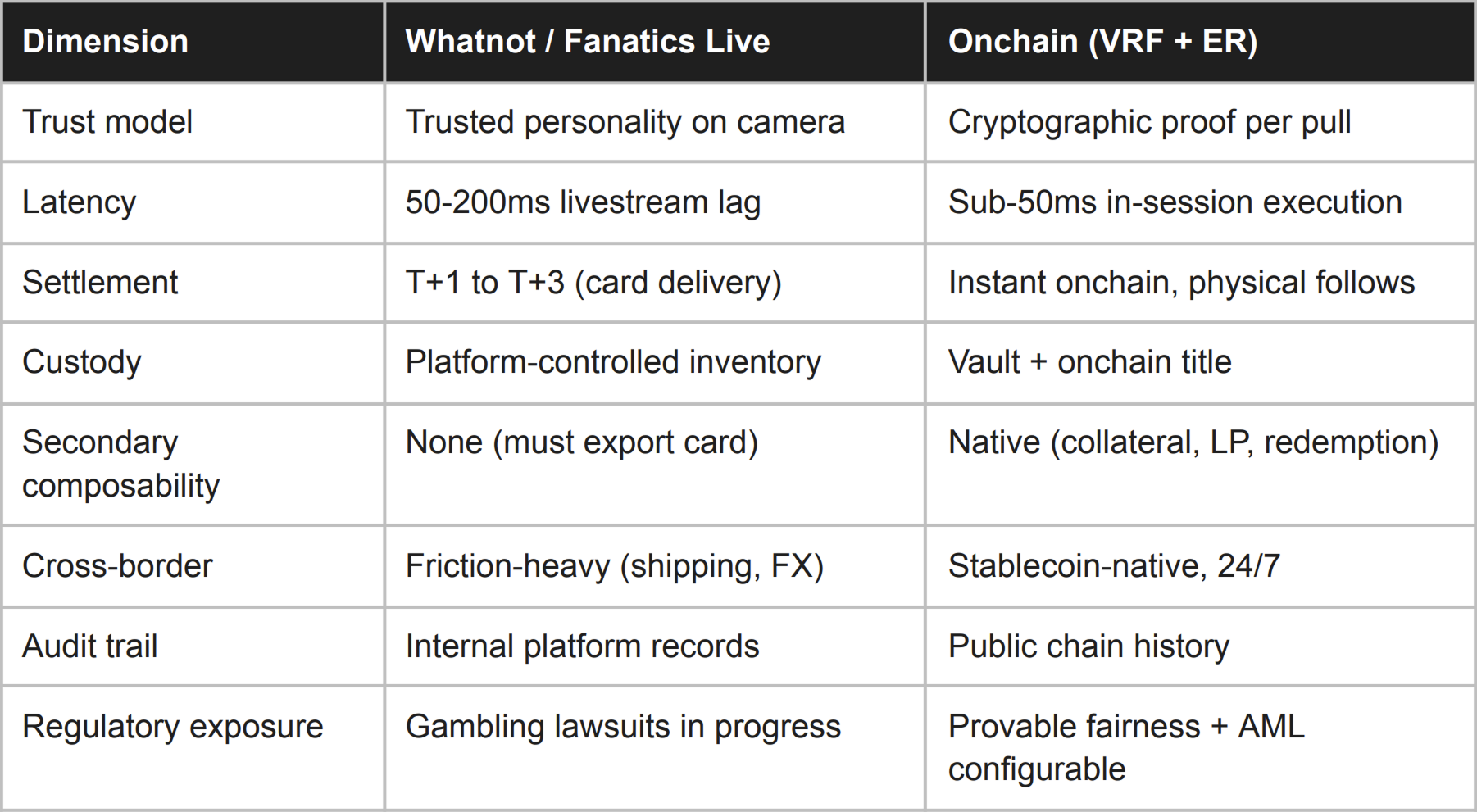

3.6 Status Quo vs. Onchain Stack

3.7 Three Horizons

Near-term (0-6 months): Live pack openings with verifiable allocation. Magic Eden plus Collector Crypt have started this with RWA Pokemon pack drops. The first projects to ship live-streamed onchain pack openings with vault-backed physical inventory and verifiable allocation capture the segment that replaces the breaker-stream model directly. Expect 3-5 new entrants in this window.

Medium-term (6-12 months): Phygital pack openings at production scale. Real-time multi-buyer pack auctions, pooled breaks with onchain settlement, asynchronous vault redemption flows. The trust layer for the $1B+ live breaking economy migrates onchain in this window.

Long-term (12-24 months): The full collectibles stack as a coordination layer. Lending against tokenized physical inventory, fractionalized exposure to high-value vaulted assets, K-pop photocard ecosystems with cross-border secondary markets, composable rarity mechanics across multiple IP holders. This is when product imagination becomes the differentiator, not infrastructure availability.

Three risks could compress these timelines. Incumbent live-stream platforms have the capital to ship internal verifiable randomness within 12-18 months, which would narrow the window onchain venues are targeting. Onchain pack opening can be classified as gambling under US state law if it isn't structured carefully. Scaling the operational stack for physical goods (vaults, insurance, logistics, customer service) is hard, and operational failures at scale could damage the category's reputation.

Conclusion

The thesis is additive: onchain extends the existing market, it doesn't replace it. Breakers will still break packs on camera, and PSA will still grade cards. What changes underneath is that pack allocation becomes provably random, ownership lives onchain, and markets connect and compose with each other while replacing trust in the operators with trust in the stack. New buyers can now participate where they couldn't inside a walled platform: cross-border collectors, lending markets, fractional traders. The market gets bigger.

Two metrics will show if this works. Onchain gacha volume on Solana is around $80M per month today. Sustained volume across multiple platforms within two quarters would signal a strong validation of the thesis. An even cleaner signal would be unique users opening packs each month, since volume can be wash-traded. If that count grows 5-10x over the same period, the consumer thesis is validated.

The behavioral demand is proven. The infrastructure is becoming ready. Replacing trusted operator with a standardized trust infrastructure is the fastest way to x10 the market from here.